Having looked at AI value creation, including rising expectations for AI and the bending of cost and revenue value creation curves, and surveyed the frontiers of engineering approaches and model innovations, the next area of focus is the investment landscape. What is the impact of these rapidly evolving business and technology shifts on investor sentiment, and what patterns relative to AI are likely to emerge for investors to pay attention to?

Seen in the context of continued strong investment enthusiasm for AI, four vectors will be worth watching. First, increased focus on AI-native companies with a concrete path toward sustained annual recurring revenue (“ARR”) growth and profitability. Second, a shift toward the customer-facing half of the AI value chain. Third, continued attention by PE firms on investments that can drive material cost efficiencies with relatively predictable applications of AI. And finally, more active exits and consolidation in the AI market.

2024 Was a Record Investment Year for AI . . . but Cautions Persist

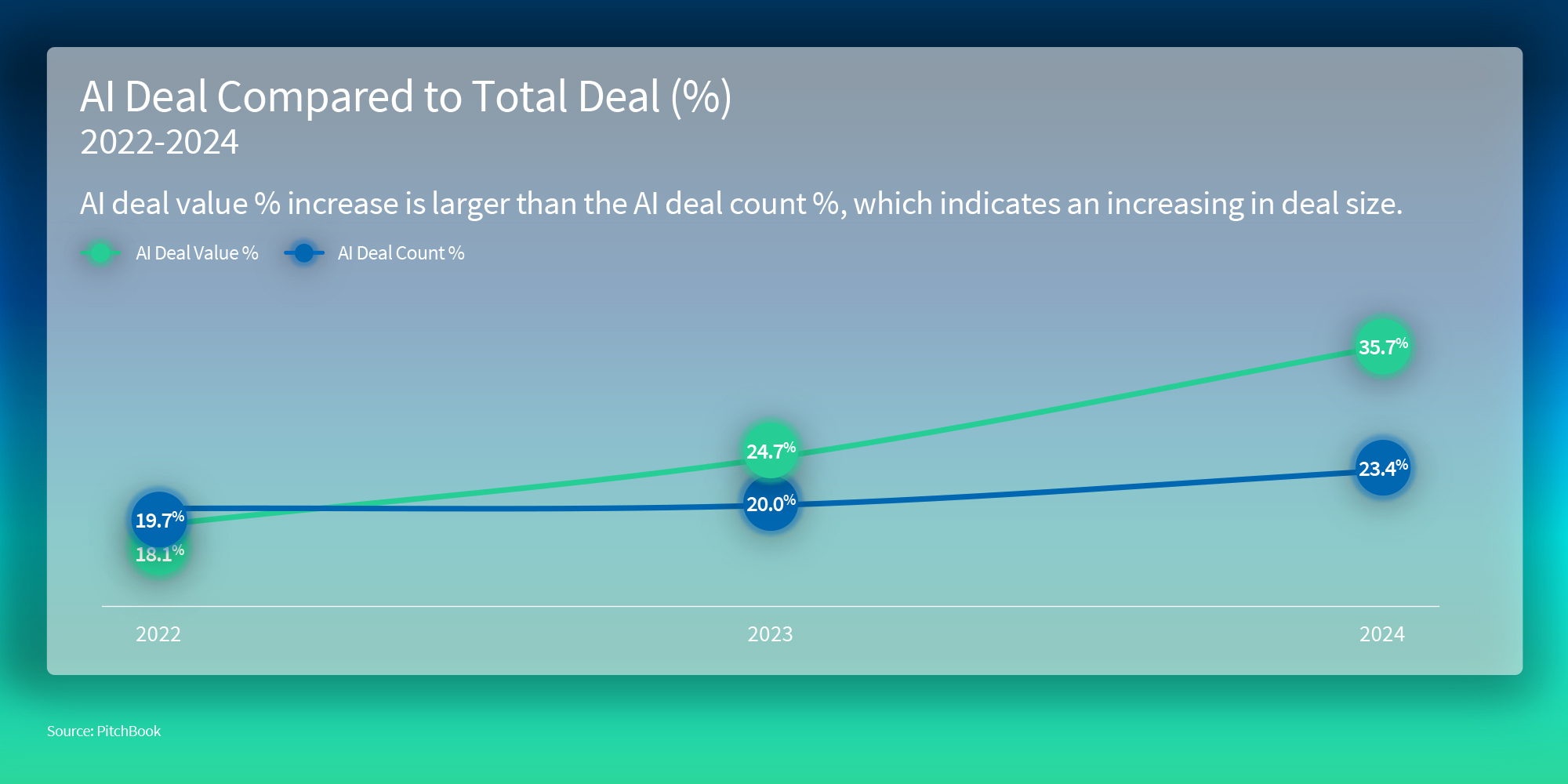

While overall venture capital (“VC”) funding was tepid, 2024 turned out to be a record year for AI investments. Although global VC investments rose to $368.5 billion in 2024 (up 5.4%), the number of deals actually fell by 17% year over year. But, interestingly, AI deals rose as a percentage of all deals. And the value of those global AI deals in 2024 was up 52%, from $86.3 billion in 2023 to $131.5 billion. AI and machine learning were 35.7% of global deal value in 2024, up from 24.7% in 2023. And AI and machine learning were 23.4% of the global deal count in 2024, up from 20% in 2023.1

Likewise, AI startups provided a jumpstart in 2024 to a U.S. VC market that had been at a secular low for years. The total capital raised in 2024 was nearly 30% higher year-on-year, and of the total $209 billion raised, AI startups captured a record 46.4%, compared to less than 10% in 2014.2

By contrast, Asia Pacific markets saw a material decline in investment activity due to the smaller amount of investment dry powder built up within the various markets across the region and the tensions between China and the U.S. government. Notwithstanding these downward pressures, some analysts see the potential of a quick reversal to this trend given that institutional investment in large-scale AI and generative AI (“GenAI”) implementations in the region are projected to reach $110 billion by 2028, growing at a compound annual growth rate (“CAGR”) of 24.0% from 2023 to 2028.4

The overall theme, then, has been the high level of capital availability for AI compared with other sectors — particularly in the United States, where one in four new startups is an AI company.5 Most of these raised multiple rounds of funding at exponentially higher valuations last year.

“Overall theme, then, has been the high level of capital availability for AI compared with other sectors — particularly in the United States, where one in four new startups is an AI company”

But there are still risks. These outsized funding rounds went to AI companies that still largely remain unprofitable, heightening the risk of unsustainable valuations, as well as the risk of “AI washing” to raise funds, given that non-AI companies have simply struggled to raise any money.

Public equity markets yield a similar picture. The forward price-to-earnings ratios (“P/E”) of the top 10 tech companies that are invested heavily in AI are running at significantly elevated levels of more than 30x compared to the S&P 500 average of 19x, a situation that last occurred during the internet dotcom period in the early 2000s. This heightened P/E multiple regime points to a risk of prices decoupling from earnings, although most of the major companies’ earnings have kept pace with prices. For AI-first tech companies to maintain such sustained P/E multiples, the larger markets need to catch up, which will only happen with a broad-based, secular consumption of AI for value creation across the corporate ecosystem over the coming years. Indeed, 1Q25 has seen significant volatility in the U.S. equity markets already, with the tech indices (e.g., Nasdaq) entering correction territory for the year.

What AI Investment Trends Can We Expect Heading Into 2025?

So, with the growing value creation potential and continuing innovation in AI model development, where will these still active AI investors place their bets in 2025? If anything, the history of tech bubbles has taught current AI investors to close their ears to the hype of “might be” and pragmatically focus on growth and profitability and on use cases that show a clear path to value.

Increasing Focus on Mid-Term ARR Growth and Profitability

AI-native companies, which are built around foundational and proprietary AI technologies, have benefited most from investor interest, and this premium will continue in 2025. High-forward multiples notwithstanding, many AI companies have shown significant revenue growth and demonstrated sustained earnings that have kept pace with price, unlike companies centered on other technology innovations such as blockchain and crypto. Expectations are that in 2025, the more robust AI-native companies will develop strong ARR, and investors will balance portfolio risk by focusing investment in those companies with clear mid-term revenue and profitability potential versus those companies with more long-term prospects.

Up until last year, it was common for us to encounter valuations in some AI sectors as high as 50x multiple of revenue due to investor enthusiasm outpacing financial performance. We expect the average valuation multiples to pull back in 2025.

Shift to the Customer-Facing Half of the AI Value Chain

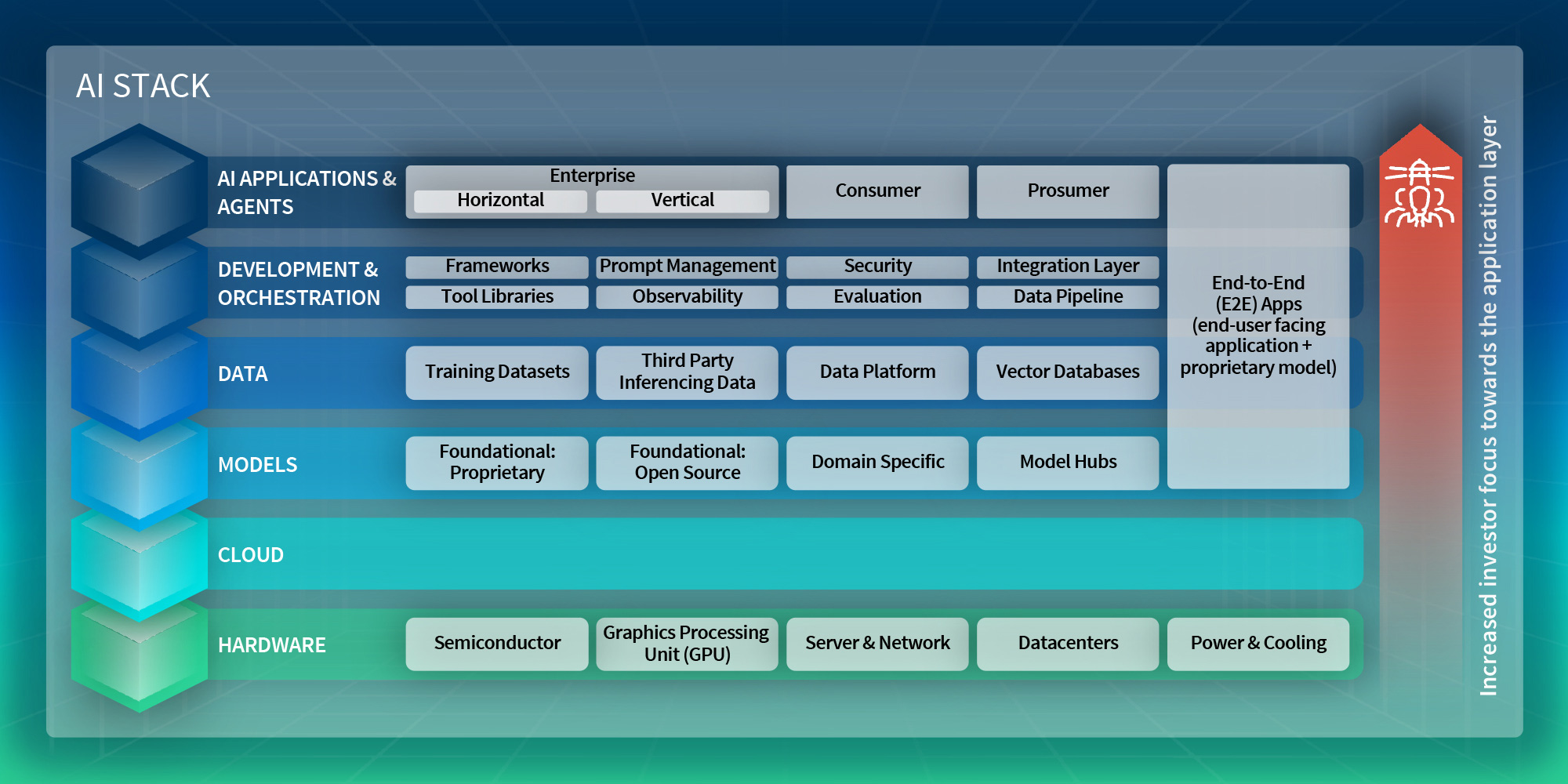

The major portion of investor activity has been concentrated thus far on the bottom half of the AI value chain — on hardware, hyperscalers and AI models. Three developments point to a coming shift. First, while investments in such AI-native companies will continue, these layers are showing signs of oversaturated investment, as represented by the forward P/E trends. Second, the AI engineering advancements discussed in our previous article, Frontiers of AI Research in 2025, point to a sign of competitive easing with model democratization and a relaxing of computational needs in the near to mid-term. Third, the history of technology revolutionary cycles points to value creation shifts to the spheres closest to the end customer and consumers — the AI-enabled products, platforms and applications that will directly simplify the human experience and the business workflows to drive profitable growth.

“History of technology revolutionary cycles points to value creation shifts to the spheres closest to the end customer and consumers”

This means that investment focus is expected to move in 2025 to the upper half of the AI stack, from training-focused investments to inferencing applications such as AI-enabled products and services.

Such investments are expected to flow along three general paths: 1) towards industry vertical applications that address EBITDA and revenue drivers for businesses in industries that stand most to gain (Chart 2 – Industry Chart) along those vectors in applying AI; 2) to horizontal enterprise functions that are currently showing the most evidence for hybrid AI approaches and improving unit economics of AI deployment to improve efficiency and effectiveness such as customer experience, R&D engineering and sales and marketing; and 3) towards AI worker frameworks and applications that provide assisted augmentation for those roles within enterprises where the need for complexity, creativity, comprehension, correctness and compliance is the lowest (Chart 4 – Roles Chart).

PE Will Focus on Pragmatic AI-Enabled Value Creation6

PE investment in AI or AI-influenced targets is on the rise. The focus in 2025 will likely be on investments that can drive material cost efficiencies with relatively predictable applications of AI. Some of the trends we are seeing on target profiles include:

- PEs acquiring companies who are either a pure play AI platform or have implemented a robust AI platform and then turning them into an investment platform play with multiple acquisitions.7 This is particularly true for businesses where AI-assisted workflows can help significantly drive down cost to serve and increase revenue per FTE.8 Some example industries are in the business process outsourcing (“BPO”), customer service and media sectors.

- The acquisition of companies that either have proper enterprise and data infrastructure that allows for AI enablement or where PEs see a clear value thesis to investment in helping the company build such infrastructure with reduction in cost to serve or the revenue gains adding up to multiples of the capital injection. Often, such companies will be in a data- or content-rich environment that enables AI use cases and can also be further monetized in other ways, such as the use of first-party customer data for AI-driven personalization that makes an investment even more attractive.

- A continuation in 2025 of significant PE investment in AI value chain enablers like data centers and in other essential staples of the AI stack like cybersecurity.9 Such investments are capital-intensive, and we are seeing evidence of PE partnerships with sovereign wealth funds, which are playing a growing role in AI investments to drive these investment cycles.

More Active Exits and Consolidation in the AI Market

We expect 2025 M&A activity within the AI sector to continue to be strong, with the likelihood of a more relaxed regulatory environment in the United States,10 a significant cash build-up by PE firms and tech companies and a strong stock price surge.

Some additional AI-specific factors also merit watching. Given the pace of growth of the AI startup market, there are some categories that may be getting saturated, leading to companies within those categories experiencing quickly narrowing strategic moats that will be spurred to contemplate an acquisition.

Conversely, if valuation multiples of AI companies begin to decline materially, as we expect to happen, many corporates who are looking to acquire AI capabilities will make strategic acquisitions of such smaller and medium companies to acquire both technical IP and talent instead of greenfield investing and building those capabilities in-house from the ground up.

Some strategic investors will seek to buy multiple assets in this fragmented market to consolidate and build more complete AI platform companies in order to leverage both product and functional synergies as well as economies of scale.

Due to these factors, we see a more heightened M&A activity in the AI sector this year and going into 2026.

Conclusion

We began this series by addressing the potential for an AI hype cycle. While that speculation may continue, investors continue to vote with their feet for AI and AI-related opportunities, but they are doing so judiciously. Perhaps informed by previous technology booms, AI-focused investors are tracking customer-focused use cases and pragmatic, nearer-term value metrics.

The blistering pace of both public and private market investments in the AI sector seen in 2024 is expected to continue into 2025, but not without continuing volatility. The rapidly evolving AI landscape and newly emerging capabilities and innovation will make placing bets on any one asset or capability a risky proposition, and investors will exhibit more discrimination, focusing on the areas of the AI value chain that will show the most reliable economic value, asset fundamentals and industry sector-specific potential.

With AI increasingly deployed in enterprises, our next and concluding piece in the series will look at the evolving challenges and risk landscape and the novel threats that have been emerging more recently.

Footnotes:

1: Nizar Tarhuni and Dylan Cox, “Q4 2024 PitchBook-NVCA Venture Monitor”, PitchBook (January 13, 2025).

2: Ibid

3: Nizar Tarhuni and Dylan Cox, “Q4 2024 PitchBook-NVCA Venture Monitor”, PitchBook (January 13, 2025). Jacob Robbins, “AI startups grabbed a third of global VC dollars in 2024”, PitchBook (January 9, 2025).

4: IDC, “Asia/Pacific* AI Investments to Reach $110 Billion by 2028, IDC Reports”, IDC (September 23, 2024), .

5: Jacob Robbins, “Nearly 1 in 4 new startups is an AI company”, PitchBook (December 24, 2024), .

6: Sumeet Gupta and Jiva J. Jagtap, “AI Takes Center-Stage for Value Creation in Private Equity Firms”, FTI Consulting Survey (2024).

7: Sumeet Gupta, Samuel Aguirre, and Carl Jones, “Assisting a Leading Global Investment Fund With Strategic Review of an Advanced AI Platform-Based Company”, FTI Consulting (February 28, 2025).

8: Sumeet Gupta, Pratyush Lal, and Carl Jones, “Creating AI Opportunities for a World-Leading Media and Technology Platform”, FTI Consulting (October 17, 2024).

9: Javier Alvarez, Edwin Grummitt, and Damilola Ojo, “How Can Sovereign Wealth Funds Navigate the AI Investment Landscape?”, FTI Delta (February 5, 2025).

10: Chuck Carroll, David Dunn, Jackson Dunn, Sumeet Gupta, John Yozzo, “Four Predictions for Private Equity in 2025”, FTI Consulting (January 25, 2025).